Abstract

This paper’s primary objective is to identify the relative impor-tance of various Islamic financial products, in theory and in prac-tice, by examining the financing records of the Bank IslamMalaysia (Berhad) and the Bahrain Islamic Bank. Currently,seven available Islamic financing products are considered viablealternatives to interest-based conventional contracts: mudarabah(trust financing), musharakah (equity financing), ijarah (leasefinancing), murabahah (trade financing), qard al-hassan (wel-fare loan), bay` bi al-thaman al-ajil (deferred payment financ-ing), and istisna` (progressive payments). Among these financialproducts, mudarabah and musharakah are the most distinct. Their unique characteristics (at least in theory) make Islamicbanks and Islamic financing viable alternatives to the conven-tional interest-based financial system.

The question before us is to determine the extent of mudarabahand musharakah in Islamic financing in practice. The data are asfollows: the average mudarabah is 5% of total financing, andthe average musharakah is less than 3%. The combined averageof mudarabah and musharakah for the two Islamic banks is lessthan 4% of the total finance and advances. The average qard al-

Abdus Samad, Ph.D., is an assistant professor in the Department of Finance andEconomics, Utah Valley State College, Orem, Utah. Norman D. Gardner, Ph.D., is a pro-fessor in the Department of Finance and Economics, Utah Valley State College, OremUtah. Bradley J. Cook, Ph.D., is vice president of Acadmic Affairs, Utah Valley StateCollege, Orem, Utah. All authors are grateful for the comments of the reviewers, whichhave added to the quality of this article.

The American Journal of Islamic Social Sciences 22:2

hassan is about 4%, while istisna` does not yet exist in practice. Murabahah is the most popular and dominates all other modesof Islamic financing. The average use of murabahah is over54%. When the bay` bi al-thaman al-ajil is added to themurabahah, the percentage of total financing is shown to be82.68%. This paper also explores some possible reasons whythese two Islamic banks appear to prefer murabahah tomudarabah and musharakah. Introduction

Islamic banking and finance are emerging as viable alternatives to conven-tional interest-based banking and financing. According to the GeneralCouncil for Islamic Banks and Financial Institutions, there are currently275 institutions worldwide that follow Islamic banking and financing prin-ciples, collectively managing in excess of $200 billion. These institutionsare spread throughout 53 countries, including Europe and the United States. Twenty institutions now offer a variety of Islamic financial services in theUnited States.

In most of these countries, Islamic banking institutions must compete

with conventional interest-based banking institutions. Their successfuloperations, along with the increasing number of Muslims in Europe andNorth America, have attracted western attention toward Islamic bankingand finance. As a result, an increasing number of western financial institu-tions now offer Islamic investment products to Muslim investors. In 1996,for example, Citi Islamic Investment Bank, a wholly owned subsidiary ofCiti Corp., opened in Bahrain; Chase Manhattan has an Islamic “window”in Frankfurt, Germany; and several multinational corporations, amongthem IBM and General Motors, have raised funds through an American-based Islamic leasing fund at the United Bank of Kuwait.

Due to the growing interest in Islamic banking in the West, a closer look

at the Islamic bank’s operations and characteristic features is warranted. Thisis the primary focus of this study.

Islamic banking in Malaysia differs in several ways, and for various

reasons, from Islamic banking in the Gulf and the rest of the world. A com-parison of Islamic banking in Malaysia and Bahrain, therefore, is valuablefor two reasons: First, Bahrain’s Islamic banking system is representativeof the best practices of Islamic banks in general, and second, Bahrain andMalaysia are currently vying for recognition as the capital or hub of Islamicbanking worldwide.

Samad, Gardner, and Cook: Islamic Banking and Finance

Islamic banking, which became established in the 1970s, currently con-

sists of a variety of financial instruments or products. These includemudarabah (trust financing), musharakah (equity financing), ijarah (leasefinancing), murabahah (trade financing), qard al-hassan (welfare loan),and istisna` (progressive payments). The relative significance of theseproducts in the Islamic banking system has yet to be studied. An addi-tional objective of this paper is to determine the extent to which these twoIslamic banks currently utilize these products. This information will beimportant to all participants in the Islamic banking and financing systems.

Review of the Literature

The extent of past scholarly research on modern Islamic banking andfinancing include studies by Siddiqi,1 Khan,2 Mannan,3 Iqbal andMirakhor,4 Ahmad,5 Zineldin,6 Saeed,7 Al-Omar and Abdul-Haq,8 andKahf.9 These authors discuss the institutional issues, including Arabic con-cepts and principles of finance that are subject to interpretation. El-Ashker,10 Wilson,11 and Kazarian12 provide financial comparisons that areuseful in understanding the Islamic financial system. Maniam, Baxely, andJames13 analyze the perception of Islamic financing in the United Statesand also discuss the problems of applying Islamic financing tools. Bacha14attributes the low growth of mudarabah financing by Islamic banks to theagency problem.

Although few empirical studies are available, Akkas15 compares Islamic

banking with conventional banking in Bangladesh, and Kazarian16 comparesit with conventional banking in Egypt. Samad17 and Samad and Hassan18compare the Bank Islam Malaysia (Berhad)’s performance with various con-ventional Malaysian banks. De-Belder and Hassan,19 as well as Hamwai andAylward,20 address some aspects of Islamic financing and its relative success. Samad21 compares the performance of interest-free Islamic banks to that ofinterest-based conventional banks with respect to profitability, liquidity risk,and credit risk.

The paper finds no major differences with regard to liquidity risk and

profitability. However, a significant difference was observed in credit per-formance. This study will contribute to the existing literature on Islamicbanking by providing data on the extent to which the various modes ofIslamic financing are actually being utilized.

The American Journal of Islamic Social Sciences 22:2

Overview of Islamic Finance and Banking

Islamic economics and financial institutions are guided by the Shari`ah, theprecepts of which are founded upon the Qur’an, the Sunnah (the practices andsayings of Prophet Muhammad [pbuh]), and fiqh (jurisprudence, the opinionof Muslim legal scholars). According to the Shari`ah, Islamic financial insti-tutions and modes of financing are based strictly on the following principles:

Transactions must be free of interest (riba’).

Goods and services that are illegal (haram) from the Islamic point ofview cannot be produced or consumed.

Activities or transactions involving speculation (gharar) must beavoided.

Zakat (the compulsory Islamic tax) must be paid.

Following is a discussion of these four principles, which make the

Islamic banking and financing system unique. INTEREST (RIBA’). Qur’an 2:185 explicitly prohibits riba’ and permits trade, but does not state clearly whether it is to be understood as interest or as usury. This lack of clarity has led to controversy among Muslim scholars in the past. However, there seems to be a general consensus that riba’ includes all forms of interest, that is, any amount charged over and above the principal.

The Islamic financial system bans interest in all transactions. Thus, the

payment or receipt of interest, which is the cornerstone of modern conven-tional banking, is explicitly prohibited in Islamic banking. Financial instru-ments and products that deal with interest are also prohibited. In otherwords, the prohibition of paying or receiving interest is the nucleus ofIslamic banking and its financial instruments.

However, it should be stated that an Islamic financial system does not

simply mean the avoidance of interest. An Islamic financial system or insti-tution is much more than that, for it “is supported by other principles ofIslamic doctrine advocating risk sharing, individuals’ rights and duties, andthe sanctity of contracts.”22 By banning interest, Islam seeks to establish ajust and fair society (Qur’an 2:239).

The return of a predetermined amount of fixed income by the lender,

irrespective of the outcome of the borrower’s venture, is considered unjust.

Samad, Gardner, and Cook: Islamic Banking and Finance

Fairness and justice demand that the owner (supplier) of capital has theright to be rewarded, but that this reward must be commensurate with thedegree of risk associated with the project for which funds are supplied. Hence, what is forbidden is the predetermined fixed charge in financing aloan, an investment, or a commodity exchange.

But there is more to the Islamic banking or financial system than just

interest-free financing For example, one must consider such factors asgharar, haram, zakat, and qard al-hassan, all of which are explained below. GHARAR. Islam prohibits all games of chance and gambling:

They will ask about intoxicants and games of chance. Say: “In both thereare great evil as well as some benefit for man, but the evil which theycause is greater than the benefit which they bring.” (Qur’an 2:219)

In Qur’an 5:90, games of chance and gambling are prohibited because theycause enmity and hatred and also involve consuming property (bay` al-batil), which is a kind of oppression.

The question is whether gharar, which involves uncertainty or specula-

tion, is halal (permitted) in business. According to Ibn Taymiyyah, if the salecontains gharar and devours the property of others, it is equivalent to gam-bling and, as such, haram (forbidden). Pointing to the phrase devours theproperty of others, Kamili23 opines that speculative risk-taking in commerce,which involves the investment of assets, skill, and labor, is not similar to gam-bling. In business, participants engage in transactions designed to maximizeprofit through trading, not through any dishonest appropriation of other peo-ple’s property. Similarly, according to El-Ashkar, speculation in business isnot the result of turning over a card or throwing the dice, but rather is

… the practice of (a) using available information to (b) anticipate futureprice movements of securities so that (c) [the] action of buying and sell-ing securities may be taken with a view to (d) buying and selling securi-ties in order to (e) realize capital gains and/or maximize the capitalizedvalue of security-holdings.24

Islam allows risk-taking in business transactions, but prohibits gam-

bling. Maniam, Bexley, and James comment:

The main idea is that investors should spend their effort searching for pro-jects that are sound, that adhere to the Shari`ah, and share in the successor failure of that project.25

The American Journal of Islamic Social Sciences 22:2

ISLAMIC INVESTMENT ETHICS. Investing in production and consumption is guided by a strict Islamic ethical code. Muslims are not permitted to invest in any production, distribution, and consumption enterprises involving alcohol, tobacco, pork, pornography, gambling, illegal drugs, and other harmful products, even though these enterprises may be profitable. In addi- tion, Islam does not permit Muslims to invest in activities that are consid- ered harmful for the individual or society. Thus, the scope of investment opportunities by Islamic banks is somewhat restricted when compared with the scope of financing open to conventional banks. ZAKAT. Zakat is a compulsory religious tax payable to the poor by those who have acquired a certain amount of wealth (nisab). Each Islamic bank must establish a zakat fund and pay this tax if the level of its earned profits reaches the level of nisab. Paying zakat does not exclude Islamic banks from paying any business-related income taxes. Thus, Islamic banks face a dual constraint: the payment of a religious tax (zakat) as well as a regular business income tax. PRODUCTS OF ISLAMIC BANKS AND THEIR KEY ELEMENTS. The prohibition of interest has led Islamic banks to create various Islamic financial instru- ments as alternatives to conventional financing methods. Based on the nature of the contracts, these Islamic financial products may be classified into two broad categories: equity-type contracts and mark-up price (debt)- type contracts. Equity-type contracts. Mudarabah (trust financing) and musharakah

(partnership), based on the profit-and-loss sharing (PLS) principle, are theonly two products that fall into equity-type contracts.26 Under a mudarabahcontract, the two parties – the supplier of capital (rabb al-mal) and theentrepreneur (trustee of the venture) – share the profits according to anagreed-upon PLS ratio. It may be 70:30 or 80:20, depending upon theagreement.

The first key element of a mudarabah contract is that the lender is not

guaranteed a specific return. There also is no fixed annual payment. This isin direct contrast to conventional interest-based lending/financing, in whicha loan is not contingent upon the profit or loss outcome of the enterprise andis normally secured by collateral. Thus, any losses must be borne by thedebtor and not the lender.

The second key element concerns losses that may arise from the busi-

ness venture. According to Maniam, Bexley, and James:

Samad, Gardner, and Cook: Islamic Banking and Finance

The financier or investor is not liable for losses beyond the capital he hascontributed, and the entrepreneur or trustee does not share in financiallosses except for the loss of his time and efforts.27

According to the Shari`ah, the supplier of capital bears the financial

loss, not the trustee (mudarib) who runs the business. The third key elementis that a financier (i.e., the Islamic bank) has no control over how the entre-preneur or trustee manages the business venture.

A musharakah underaking is a partnership contract between two or

more parties, each of which contributes investment capital. In a conven-tional sense, it is a joint business contract.

The first element of a musharakah contract is that both parties con-

tribute capital investment and that profits are shared by a prearranged agree-ment, not necessarily in proportion to their invested capital. In case of loss,both parties share in proportion to their capital contribution. The second ele-ment is that both parties share and control how the investment is managed. Thus, the Islamic bank has the right to examine the enterprise’s books andsupervise its management. The third element is that liability is unlimited. “Therefore,” write Maniam, Bexley, and James, “each partner is fully liablefor the actions and commitments of the other in financial matters.”28

Given the above factors, both mudarabah and musharakah have ele-

ments of equity financing. The Islamic bank, as a supplier of funds,undertakes joint ventures with individual customers. Such a relationship isprohibited in the conventional banking system.

Mark-up price (debt)-type contracts. The basic principle of mark-up

contracts is that the bank finances the purchase of assets in exchange for anegotiated profit margin. Two of the five instruments in this category arewidely used. Murabahah (Cost-plus-profit margin). Murabahah (bay` bi al-thamanal-ajil) is a cost-plus-profit margin contract whereby the Islamic bank pur-chases an asset on behalf of an entrepreneur and resells it to him/her at apredetermined price. This latter price includes the cost of the asset plus anegotiated profit margin. Under this contract, payment is made to the bankin the future either in a lump sum or in installments.

The key characteristic of a murabahah contract is that ownership of the

asset remains with the bank until all of the payments have been made. Thisis a popular substitute for interest-based conventional trade financing.29From an economic point of view, murabahah financing and interest-basedtrade financing appear quite similar, except in their contractual features.

The American Journal of Islamic Social Sciences 22:2

Ijarah (Lease financing). Ijarah involves acquiring the financing

needed to use a particular asset. In such a contract, the Islamic bank pur-chases an asset on behalf of the entrepreneur and allows him/her to use itfor a fixed rental payment. In ijarah bi tamlik or ijarah wa iqtina` (leasefinancing toward eventual ownership) financing, the Islamic bank buys anasset and leases it to the entrepreneur, who eventually opts to buy it at a pre-viously agreed-upon price. The key characteristic of ijarah is that owner-ship of the asset remains with the Islamic bank or is gradually transferredto the entrepreneur as the lease payments are made.

The Islamic bank has other financial products, such as bay` bi al-thamanal-ajil (deferred payment financing) and istisna` (progressive payment). These debt-like products fall into the category of a “cost-plus” contract. Akey characteristic of these contracts is that ownership of the asset unam-biguously remains with the bank until all of the payments have been made. Qard al-hassan (Benevolence loan). Qard al-hassan, a unique product

of the Islamic bank, is a zero-return loan (a negative investment). AllIslamic banks are urged or required to make these benevolence loans toneedy and poor people. There is no financial return on this loan, for the bor-rower is obligated to repay only the principal.

We will now discuss the relative importance of these instruments in

practice by examining the financing records of two Islamic banks: one inBahrain and the other in Malaysia. We examine how they use the funds asthey provide financing to their customers. Data and Methodology

We have selected two Islamic banks for study: the Islamic Bank of Bahrainand the Bank Islam Malaysia (Berhad). These two banks were selected forseveral reasons:•

Both Bahrain and Malaysia provide relatively open access to bankinformation.

Both banks operate in well-developed financial markets and competewith conventional financial centers and offshore banks.30

Both banks operate according to the Shari`ah and compete with con-ventional banks, some of which also offer Islamic financial instrumentsto their customers but are not bound by the Shari`ah.

While the relative importance of the various Islamic financial productsmay well differ in banks operating in Iran and Sudan, where all busi-

Samad, Gardner, and Cook: Islamic Banking and Finance

nesses and banks must comply with the Shari`ah, the two Islamic banksexamined here are considered more representative of banks that arecompeting with conventional banks throughout the rest of the Muslimworld.

The data for the Islamic Bank of Bahrain and the Bank Islam Malaysia

(Berhad) were obtained from their 2002 annual reports. We have simplycalculated the relative percentages of the various modes of financing usedby them.

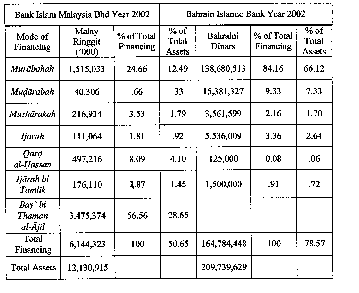

The asset side of the balance sheets of the Bank Islam Malaysia (Berhad)and the Bahrain Islamic Bank, as presented in table 1, demonstrates theimportance of the various Islamic financing modes. As we can see, totalIslamic financing and advances by the Bank Islam Malaysia (Berhad) isonly 50.65% of the total assets. On the other hand, the total Islamic financ-ing by the Bahrain Islamic Bank is 78.57%. On average, the total Islamicfinancing for the two Islamic banks was 64.61% of assets.

Table 1. Allocation of Funds under Finance and Advances.

The American Journal of Islamic Social Sciences 22:2

Earlier in this paper, we established that mudarabah (trust financing)

and musharakah (equity financing) are the pillars or foundations of theIslamic banking system. When the breakdown of the total allocation pre-sented in table 1 is examined, it appears that both of them play virtuallyno role in these two Islamic banks, as compared to other modes of financ-ing. For the Bank Islam Malaysia (Berhad), mudarabah accounts for only.66% of total financing; for the Bahrain Islamic Bank, it constitutes 9.33%of total financing. On average, mudarabah in these two Islamic banks isonly 5%.

The other distinguishing Islamic financing instrument is the musha-rakah contract. In these two Islamic banks, as the data show, this financingmode is also insignificant: It is 3.53% (Malaysia) and 2.16% (Bahrain),respectively. On average, it constitutes only 2.85% of total Islamic financ-ing. Even though musharakah appears to be very significant in principle, inpractice it constitutes an insignificant proportion of Islamic financing inthese two banks. Adding together the two bank’s average mudarabah andmusharakah financing, the total is only 3.92% of total financing. Thus, thetwo most notable Islamic products are seen, in practice, to constitute lessthan 4% of their total Islamic financing instruments.

With regards to murabahah (debt-like financing contracts), the data in

table 1 show that such financing in Malaysia and Bahrain is 24.16% and84.16%, respectively. On average, murabahah financing is 54.41% of totalfinance and advances. It should be noted that if the figures for murabahahand bay` bi al-thaman al-ajil are added together for the Bank IslamMalaysia (Berhad), the percent of total financing is 81.2%. This percent-age compares favorably with that listed under murabahah for the BahrainIslamic Bank (84.16%). No amount is shown under bay` bi al-thaman al-ajil for the Bahrain Islamic Bank. Aggregating the figures for these twotypes of financing is understandable, since their characteristics are quitesimilar. The average of total financing of these two Islamic banks undermurabahah and bay` bi al-thaman al-ajil is 82.68%. From the point ofview of some critics, murabahah is not a pure Islamic product;Nevertheless, the data show this mode of financing is dominant in theIslamic banks of Malaysia and Bahrain. Qard al-hassan (benevolence/philanthropic) financing is another cor-

nerstone of Islamic finance, for helping the poor and needy is a fundamen-tal Islamic teaching. The extent of participation in this mode of financingwas considered and found to be 8.09% in Malaysia and only 0.08% inBahrain. This difference is probably due to the larger proportion of needy

Samad, Gardner, and Cook: Islamic Banking and Finance

people in Malaysia and the increased availability of governmental assis-tance for the needy in Bahrain. The average qard al-hassan financing bythe Bank Islam Malaysia (Berhad) and the Bahrain Islamic Bank is only4.09% of the total finance and advances.

The data on ijarah (general lease financing) show that the average

ijarah financing of the two Islamic banks under discussion is 2.59% of theirtotal finance and advances. With regard to the new Islamic financing instru-ment of istisna` (progressive payment), their balance sheets indicate noallocation. This suggests that they have not yet participated in this mode offinancing. Given this, we can say that this new instrument appears to existin theory but not yet in practice.

Zakat, a compulsory religious tax, is one of the five pillars of Islam that

both individuals and businesses are required to observe. Therefore, Islamicbanks are obligated to pay it as an integral part of Islamic finance. Anexamination of these two Islamic banks’ income statements reveals that theBank Islam Malaysia (Berhad) and the Bahrain Islamic Bank pay a zakatof RM 1,125,000 (6.13% of the total profit) and BD 1,341,555 (1.69% ofthe total profit), respectively, from their operating profits. It should be notedthat both of these banks operate under the conventional business laws oftheir respective countries and thus pay this religious tax in addition to theconventional income tax.

In theory, mudarabah and musharakah constitute the foundation of the

Islamic financial system. Nevertheless, the data presented here seem toindicate that they are utilized far less than other forms of Islamic financing,such as murabahah. Some possible explanations as to why these instru-ments are not utilized to a greater extent are discussed below.

When a business is run by professional managers, as opposed to the owneror supplier of capital (debtholder or shareholder), a conflict of interest mayarise. A manager is the business owner’s agent. As the utility increases, man-agers will seek to maximize their own utility instead of maximizing thewealth or utility of the shareholders or the business owners. They have anincentive to increase their own salaries, fringe benefits, and other perks, allof which represent a conflict of interest that may lead them to place per-sonal interest ahead of such corporate goals as maximizing the shareholders’profit margin.31 This conflict is the most common problem in all businessesor corporations managed by agents rather than the shareholders or debthold-

The American Journal of Islamic Social Sciences 22:2

ers themselves.32 Given its prevalence, it is important to see how it applies tomudarabah and musharakah. THE AGENCY PROBLEM IN MUSHARAKAH FINANCING. Earlier in this paper, musharakah was described as essentially a joint venture profit-sharing business of two or more parties in which the Islamic bank is an important partner or shareholder. Under musharakah, the bank relies on the other partner(s) to manage the business and make the day-to-day decisions. Even though the bank could monitor the management of the business by hiring external auditors and consultants, such measures would incur additional costs. Therefore, the bank must rely on professional managers or other part- ners to manage the businesses, even though these managers may have an incentive to maximize their own utility at the business owner’s expense. THE AGENCY PROBLEM IN MUDARABAH FINANCING. As Bacha states: “Muda- rabah financing is really a hybrid. It is neither equity nor debt, because it has important features of both.”33 This type of financing has elements of equity financing, since the Islamic bank receives no fixed annual return. In fact, such a return from the business is similar to a dividend, which the busi- ness pays only if it earns a profit.

On the other hand, mudarabah has elements of conventional debt

financing, because in the event of dissolution, the bank has a “fixed” claimon the venture equal to the initial capital provided, plus its share of any prof-its. Under mudarabah, the Islamic bank does not participate directly in man-agement decisions. Rather, it relies completely on the business venture’strustee or entrepreneur. This trustee is clearly an agent of the Islamic bankand, therefore, is inherently subject to the agency conflict of interest.

Thus, under both musharakah and mudarabah, the Islamic bank expe-

riences the agency problem with its associated costs. Islamic banks oper-ate primarily in developing countries, where there is a high degree offinancial market imperfection and a prevailing presence of inefficiency andcorruption.34

The agency problem becomes more acute when banks have little access

to dependable accounting information, due to a lack of standardized finan-cial reporting requirements and procedures. The difficulties presented bythis agency problem, together with the lack of verifiable financial data,complicate the profit-sharing characteristics of these forms of Islamicfinancing and actually encourage debt financing (e.g., murabahah andijarah) over equity financing (e.g., musharakah and mudarabah).35

Samad, Gardner, and Cook: Islamic Banking and Finance

To some extent, the agency problem in musharakah and mudarabah

can be reduced by carefully specifying the sharing of profit and perfor-mance bonuses between the entrepreneur and the bank. Also, in the case ofmusharakah, the bank participates in the election of the company’s boardand officers, a factor that should further reduce the agency problem.

AMBIGUITY IN ASSETS OWNERSHIP. In mudarabah and musharakah, some ambiguity exists concerning the title to assets in case of default or dissolu- tion of the business. Under murabahah and ijarah, there is no such ambi- guity. In these debt-type contracts, title to the assets clearly remains with the bank until all payments have been made. Under a PLS contract, how- ever, banks have no direct claim on the financed assets. As a result, it is rational for banks to opt for murabahah and ijarah contracts instead of mudarabah and musharakah contracts. In order to partially offset the increased risk of musharakah and mudarabah contracts, the business assets could be registered under the joint or co-ownership concept provided by a partnership or corporation arrangement.

It should be noted here that a western debt contract contains a consider-

able amount of ambiguity over just who controls the assets in the case ofdefault. In western countries, default triggers bankruptcy proceedings, duringwhich the entrepreneurs and the managers may continue to control the assetsof the business. In contrast, there is no such ambiguity in the case of mura-bahah and ijarah contracts: The bank may seize the assets immediately.

CONTRACT MATURITY. Contrary to mudarabah and musharakah, mura- bahah financing constitutes a shorter term, lower risk investment for the bank. This form of financing involves buying goods at a low price and sell- ing them immediately at a higher price. Such contracts require a specific payment schedule with known maturities. In contrast, the equity nature of mudarabah and musharakah contracts results in longer term, more uncer- tain maturities for these investments. These differing risk characteristics may bias the Islamic bank against mudarabah and musharakah financing. Primary data collected by Samad and Hassan36 from the Malaysian Islamic Bank (Berhad) support this finding. PRIVACY AND CONFIDENTIALITY. Entrepreneurs are, in general, independent, free-spirited people who jealously guard their proprietary information. Since joint management and supervision are important characteristics of musharakah financing, entrepreneurs may not view such requirements pos-

The American Journal of Islamic Social Sciences 22:2

itively. Nevertheless, both mudarabah and musharakah require that thebank be given detailed knowledge of how the businesses they finance oper-ate and be allowed to participate in all management decisions. This situa-tion is likely to cause concern among those entrepreneurs who prefer tokeep the details of their business operations private. Information on operat-ing procedures and the degree of profitability is not usually shared will-ingly by entrepreneurs, who are concerned about competitors entering themarketplace. Such concerns may well decrease the demand for mudarabahand musharakah financing. BIASED BANK PERSONNEL. Another possible impediment to a more rapid growth of mudarabah and musharakah may lie with the Islamic bank man- agers themselves. Islamic banks are currently managed by people who have been educated and trained in the conventional banking system. Thus, more time may be required for the unique characteristics of Islamic financial instruments to be completely accepted and understood by both bank per- sonnel and customers. A similar observation is found in the study by Maniam, Bexley, and James.37 INVESTMENT CONSTRAINTS. As noted earlier, the Shari`ah restricts the type of businesses for which Islamic banks can provide financing. For example, they are not permitted to participate in certain prohibited investments or joint venture projects considered to be detrimental to the individual, society, or the environment. As a result, the scope of mudarabah and musharakah for Islamic banks is somewhat more limited than it is for conventional banks. A LONG RECORD OF ESTABLISHED RELATIONS. Even though Muslims through- out the world could be expected to prefer to deal with an Islamic bank for purely religious reasons, the fact is that prior to the 1970s, when no Islamic banks were available, they dealt with conventional banks. Thus, banking relationships have already been established and, except for that segment of the banking community that is so religious that its members could be expected to transfer all of their banking transactions to the first available Islamic bank, others who would prefer the Islamic bank (if all else were equal) may base such decisions more on the relative economic advantage to them as consumers.

Therefore, it would seem incumbent upon Islamic banks to price their

instruments in a way that the customers’ net position is as current and com-

Samad, Gardner, and Cook: Islamic Banking and Finance

petitive as it is in the conventional banks. When the net economic conse-quences of being a customer of an Islamic bank are substantially the sameas those associated with conventional banks, it could be expected that thereligious preference of the majority of banking customers would attractthem to Islamic banks and their Islamic financing instruments.

COMPETITION FROM CONVENTIONAL BANKS. Islamic banks compete with conventional banks in both the deposit and credit markets. Some conven- tional banks, such as the Bank Bumiputra Malaysia Berhad, have intro- duced Islamic deposit instruments, thereby increasing the competition for funds. As a result of this increased competition, Islamic banks are finding it difficult to attract significant funds in the form of mudarabah deposits, a factor that further limits the growth of mudarabah and musharakah financ- ing. Available data on the Bank Islam Malaysia (Berhad) reveal that of the total customer deposits of RM 11,056,355, the amount of mudarabah deposits was only RM 250,992 – a mere 2.27% of total deposits. Conclusion

The above examination of the balance sheets, finance and advances, andincome statements of two Islamic banks in Malaysia and Bahrain disclosesthat Islamic banks follow the Shari`ah’s injunction to pay zakat and financeeconomic activities through Islamic contracts. Among these financial con-tracts, mudarabah, musharakah, qard al-hassan, and istisna` are the mostdistinguishing products in the theory of Islamic finance. However, the dataindicate that for the two Islamic banks studied here, mudarabah, musha-rakah, and qard al-hassan financing are the least significant financial instru-ments. The average level of mudarabah financing engaged in by these twoIslamic banks is only 5%, and for musharakah it is less than 3%, making thecombined average less than 4% of total finance and advances. The averagefinancing under the qard al-hassan (benevolence) mode is about 4%. Istisna` (progressive) is not yet used by these two Islamic banks.

Mark-up products, such as murabahah and ijarah, appear to be the

most popular, for they dominate all other modes of Islamic financing. Theaverage murabahah financing for these two Islamic banks is over 54%. When bay` bi al-thaman al-ajil and murabahah are considered together, theaverage financing of these two Islamic banks is 82.68%. These figures aresignificantly higher than the combined mudarabah, musharakah, and qardal-hassan financing (less than 12%). Further research should be conducted

The American Journal of Islamic Social Sciences 22:2

to investigate the extent to which mudarabah and musharakah are utilizedin other Islamic countries.

It is understandable that, during the initial development of the Islamic

banking system, musharakah and mudarabah financing should be de-emphasized due to the increased risk associated with them. Nevertheless,we can expect that these Islamic financial instruments will increase inimportance as the Islamic banking system continues to mature. Endnotes

M. N. Siddiqi, Issues in Islamic Banking (Leicester: Islamic Foundation,1983).

S. R. Khan, Profit and Loss Sharing: An Islamic Experiment in Finance andBanking (Karachi: Oxford University Press, 1987).

M. A. Mannan, “Islam and Trends in Modern Banking: Theory and Practiceof Interest-Free Banking,” Islamic Review and Arab Affairs (November/December 1998): 73-95.

Z. Iqbal and A. Mirakhor, “Progress and Challenges of Islamic Banking,”Thunderbird International Business Review 3 (1999): 381-403.

Ausaf Ahmad, Development and Problems of Islamic Banks (Jeddah: IslamicDevelopment Bank, Islamic Research and Training Institute, 1987).

M. Zeneldin, The Economy of Money and Banking: A Theoretical andEmpirical Study of Islamic Interest-free Banking (Stockholm: Almqvist &Wiksell International, 1990).

M. Saeed, Islamic Banking and Interest (Leiden, the Netherlands: E. J. Brill,1996).

F. Al-Omar and M. Abdel Haq, Islamic Banking: Theory, Practice andChallenges (Karachi: Oxford University Press, 1996).

M. Kahf, “Islamic Banks at the Threshold of the Third Millennium,”Thunderbird International Business Review 3 (1999): 445-59.

10. A. A. El-Ashker, The Islamic Business Enterprise (New Hampshire: Croom

11. R. Wilson, Islamic Financial Markets (New York: Routledge, 1995). 12. E. G. Kazarian, Islamic Versus Traditional Banking: Financial Innovation inEgypt (Colorado: Westview Press, 1993).

13. B. Maniam, James J. Bexley, and Joe F. James, “Perception of Islamic

Financial System: Its Obstacles in Application, and Its Market,” Academy ofAccounting and Financial Studies Journal 4, no. 2 (2000): 22-36.

14. Obiyathulla Ismath Bacha, “Conventional versus Mudarabah Financing: An

Agency Cost Perspective,” Journal of Islamic Economics 4, nos. 1-2, (1995):33-49; De Belder, R. K. and M. Hassan, “The Changing Face of the IslamicBanking,” International Financial Law Review 1 (1993): 23-26.

Samad, Gardner, and Cook: Islamic Banking and Finance

15. Ali Akkas, “Relative Efficiencies of the Conventional and Islamic Banking

System in Financing Investment” (unpublished Ph.D. diss., DhakaUniversity, Dhaka, Bangladesh, 1996).

16. Kazarian, Islamic Versus Traditional Banking. 17. Abdus Samad, “Comparative Efficiency of the Islamic Bank vis-à-vis

Conventional Banks in Malaysia,” Journal of Management and Finance 7, no. 2 (1999): 1-24.

18. Abdus Samad and M. Kabir Hasan, “The Performance of Malaysian Islamic

Bank during 1984-1997: An Exploratory Study,” Thoughts on Economics 10,nos. 1-2 (2000): 7-26.

19. R. K. De Belder and M. Hassan, “The Changing Face of Islamic Banking,”

International Financial Law Review 1 (1993): 23-26.

20. B. Hamwi and A. Aylward, “Islamic Finance: A Growing International

Market,” Thunderbird International Business Review 3 (1999): 407-20.

21. Abdus Samad, “Performance of Interest-free Islamic Banks vis-à-vis Interest-

based Conventional Banks,” IIUM Journal of Economics and Management12, no. 2 (2004): 115-29.

22. Z. Iqbal and A. Mirakhor, “Progress and Challenges,” 39723. M. H. Kamali, “Islamic Commercial Law: An Analysis of Futures,” AmericanJournal of Islamic Social Sciences 13, no. 2 (1996): 197-224.

24. A. F. El-Ashkar, “Towards an Islamic Stock Exchange in a Transition Stage,”

Islamic Economic Studies 3, no. 1 (1995): 89.

25. Maniam, Bexley, and James, “Perception,” 25. 26. Hamwi and Aylward, “Islamic Finance.”27. Maniam, Bexley, and James, “Perception,” 26. 28. Ibid. 29. M. Josh, “Islamic Banking Rises Interest,” Management Review 2 (1997): 25-

30. Laubon and Manana are important centers of offshore banking in Malaysia

31. Jensen and Meckling have identified significant costs associated with the

agency problem. M. C. Jensen and W. H. Meckling, “Theory of the Firm:Managerial Behavior, Agency Costs and Ownership Structure,” Journal ofFinancial Economics 3 (1976): 305-60.

32. In a landmark study, Lewellen found that in the American financial system,

this agency problem has been largely mitigated by the use of executive stockoptions. These stock options provide the incentive for managers to maximizeshareholder wealth, and thus significantly reduce the agency problem. WilburG. Lewellen, “Management and Ownership in the Large Firm,” Journal ofFinance (May 1969): 299-322.

33. Bacha, “Conventional versus Mudarabah Financing,” 40. 34. Paolo Mauro, “Corruption and Growth,” Quarterly Journal of Economics

The American Journal of Islamic Social Sciences 22:2

35. Oliver Hart and John Moore. “Default and Renegotiation: A Dynamic Model

of Debt,” Quarterly Journal of Economics 113 (1998): 1-41.

36. Samad and Hasan, “Performance.”37. Maniam, Bexley, and James, “Perception.”

Original Publications (Takehiko Kamijo, M.D., Ph.D.) 1. Ichikawa M, Yanagisawa M, Kawai H, Kamijo T, Komiyama A, Akabane T Spontaneous improvement of juvenile rheumatoid arthritis after T lymphocytosis with suppressor phenotype and function. J Clin Lab Immunol. 1988 Dec;27(4):197-201. 2. Kamijo K, Kamijo T, Ueno I, Osumi T, Hashimoto T Nucleotide sequence of the human 70 kDa peroxisom

The Dachshund Back Digest This is a digest of several articles written by members of the "Dachshund-L" and "dachsies@" mailing listsin response to inquiries about Dachshund back problems. There are also some case histories and submittalsfrom authors which did not appear on the lists. None of the authors are veterinarians, the information shouldonly be regarded as opinions of

Samad, Gardner, and Cook: Islamic Banking and Finance

nesses and banks must comply with the Shari`ah, the two Islamic banksexamined here are considered more representative of banks that arecompeting with conventional banks throughout the rest of the Muslimworld.

Samad, Gardner, and Cook: Islamic Banking and Finance

nesses and banks must comply with the Shari`ah, the two Islamic banksexamined here are considered more representative of banks that arecompeting with conventional banks throughout the rest of the Muslimworld.